Building for the Next Generation: A Workers’ Strategy for Canada’s Aerospace Industry

![]()

Foreword

Canada’s aerospace industry boasts a history of remarkable achievements and holds immense potential for future growth. However, to navigate the challenges ahead and capitalize on opportunities, a unified strategic approach is essential.

Globally, demand for civil, search and rescue, firefighting and defence aircraft is growing rapidly. The space industry, which includes satellites in low-earth orbit and space exploration technology is expected to grow significantly in the next decade. Research and development (R&D) focussed on new technology to reduce emissions and meet the next generation of aerospace challenges is already in full swing.

Canada has all of the ingredients necessary to grow the aerospace industry to fulfill global demand. Canada’s highly skilled aerospace workforce is a coveted resource the world over. Canada is one of only a handful of country’s home to all the capabilities needed to build an aircraft from the design stage to final assembly. The country has a world-class R&D ecosystem and, in Transport Canada, a highly respected regulator that is trusted to certify aircraft for international operation.

Canada cannot let this opportunity go to waste. Government, unions, academia and aerospace companies must act in a coordinated effort to ensure Canada maintains its status as a prime location for R&D, production and maintenance, repair and overhaul (MRO) activities. Canada must ensure the aerospace industrial ecosystem is able to consistently create the next phase of the industry for the next generation.

The aerospace industry is a crown jewel in Canada’s industrial economy and the benefits it delivers are highly sought after. Good jobs requiring substantial skill that offer decent pay and good benefits are high on the list of priorities for Canada’s economy. Innovation and economic growth are just as high. All of these are co-created by aerospace industry stakeholders. With focussed intentions and a concerted effort from all parties, the aerospace industry can deliver on Canada’s many economic goals.

All over the world, countries are developing comprehensive strategies to attract aerospace manufacturing investments from Original Equipment Manufacturers (OEMs) and major industry suppliers. If Canada does not follow suit not only will the country lose out, it will put the good jobs and economic benefits currently supported by the industry at risk including tens of thousands of direct jobs, leading R&D spending in advanced manufacturing, a favourable trade balance and productive capacity.

This document outlines Unifor’s vision for the aerospace sector and puts forward several industrial policy recommendations to respond to present and upcoming challenges identified within the industry. Centred around 4 main pillars, these propositions address the need for a national strategy, increased collaboration among stakeholders, worker attraction, training and adaptation, industry supports, public procurement and funding. All recommendations are underwritten by a common goal: to create a vibrant aerospace ecosystem sustained by a resilient workforce that benefits from good jobs.

Table of Contents

-

Introduction

Building the Next Phase of Canada’s Aerospace Legacy -

Unifor in the Aerospace Sector

Unifor membership across Canada (visual layout) -

Canada’s Aerospace Industry by the Numbers

Key Industry information and metrics (visual layout) -

Pillar 1: Strategic framework and stakeholder collaboration

The Case for a National Aerospace Industrial Strategy -

Pillar 2: Workforce attraction, training and adaptation

Attracting and Retaining the Next Generation of Aerospace Workers

Supporting a World-Class Aerospace Education and Training Programs

Ensuring Technological Changes and AI Integration Benefit Workers -

Pillar 3: Ecosystem Supports and Made-in-Canada Solutions

Supporting and Expanding the Canadian Aerospace Industrial Ecosystem

Using Public Procurement to Strengthen the Aerospace Industry -

Pillar 4: Investments and Funding Programs

Providing Canada’s aerospace industry with targeted and flexible funding

Introduction

Building the Next Phase of Canada’s Aerospace Legacy

For over a century, the Canadian aerospace industry has attained some remarkable achievements. The first motorized flight of the Silver Dart in 1909 in Baddeck Bay, Nova Scotia marked the beginning of an adventure in which Canada has often been a trailblazer. From the Anouk and Alouette satellites to the PT6 turboprop engine, the CanadArm and C-Series aircraft (now known as the A220), these industrial successes in aerospace are a testament to Canadian ingenuity and a reflection of the major technical capability and experience and skill of thousands of workers.

Globally, the aerospace industry, which is made up of three main sub-industries: civil aviation, space, and search, rescue and defence, is poised for substantial growth in the coming decade. Consumer air travel has returned to pre-pandemic levels; air cargo activity soared during the pandemic and remains a stronger contributor to the industry than before the pandemic; governments are poised to spend billions of dollars on aircraft and satellites that will be used in a wide range of missions, from monitoring climate change to protecting national borders; and the space sector has transitioned from a niche market to a global powerhouse of fast-evolving products and services.

The civil aircraft market alone is expected to generate $3.9 trillion (USD) of economic activity between now and 20421. Experts predict that the space industry will grow to $1.8 trillion by 2035 as it moves from a niche market to holding a ubiquitous, if often invisible, presence in the lives of Canada’s people2. All of this while the global defence industry continues to expand. Canada’s Department of National Defence has committed $73 billion over the next 20 years to defence capabilities and activities that will include aerospace-related equipment.

Canada is in a unique position to benefit from these developments but as the global competitive landscape transforms it must do more to protect its industrial assets and ensure it is well positioned to take advantage of future opportunities.

In order to fully harness this potential, Canada’s actions must be informed by a dedicated strategic framework that it currently does not have. The country needs a national aerospace industrial strategy that identifies gaps, sets clear and attainable goals, channels resources towards priorities based on key strengths, and fosters collaboration among stakeholders.

Taking Stock of the Challenges

In 2023, Canada ranked among the top five countries in the manufacture of flight simulators, engines and civilian aircraft. Internationally, the Canadian aerospace industry ranks sixth, after the United States, the United Kingdom, China, France and Germany in size. In the early 2000s, it was fourth.

Today, the Montreal area is the third leading aerospace hub in the world, after Seattle and Toulouse. It is one of the rare places in the world that brings together the expertise needed to carry out every stage of production of an aircraft, from the drawing board to certification but it faces stiff competition from other fast-growing regional clusters in the U.S., China, India, and elsewhere.

Many countries covet Canada’s advanced aerospace manufacturing sector, which has the ability to mobilize an entire research ecosystem, create good jobs and contribute to a healthy trade balance. Several industrial powers, both emerging and established, have set their sights on Canadian aerospace assets. On the global stage, key players from China to the U.K. have recently introduced fulsome industrial policies and continue to make substantial investments in key development areas.

In addition to this growing competition, the industry is operating in an environment that is marked by increased instability and complexity: labour shortages, accelerated technological development cycles, supply chain disruptions, production relocation, protectionist measures, geopolitical turmoil, climate change and more. A national aerospace industrial strategy focussed on good jobs, a skilled workforce, investment attraction and made-in-Canada solutions could help mitigate some of these challenges.

Worrying Trends

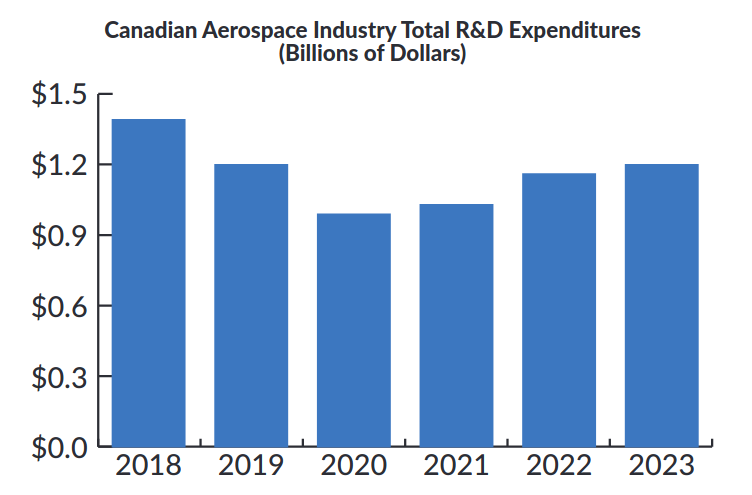

The 15% decrease in R&D spending between 2018 and 2023 is cause for concern. The aerospace industry was responsible for one quarter of all R&D spending in the manufacturing sector in Canada in 2017. At that time, R&D spending in the sector was 7 times as intensive compared to the manufacturing industry overall. In 2023 R&D intensity – the ratio of a company’s research and development spending to its total sales or revenue – compared to the rest of the manufacturing was only 2.3. The decline signals a loss of momentum. The importance of this type of spending cannot be overstated. It is a catalyst for industrial innovation that underpins Canada’s excellence in the sector.

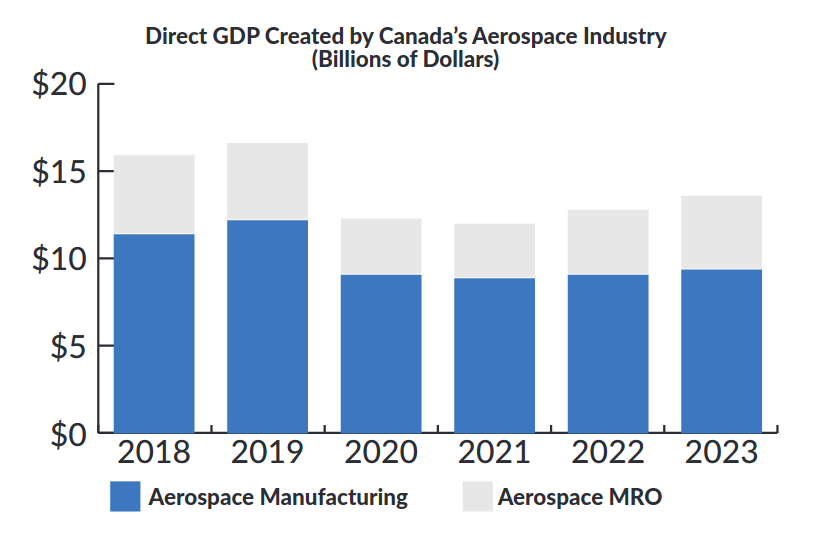

Similarly, GDP and revenue created by the industry declined dramatically during the first year of the pandemic. By the end of 2023, aerospace GDP was still 20% lower than 2018.

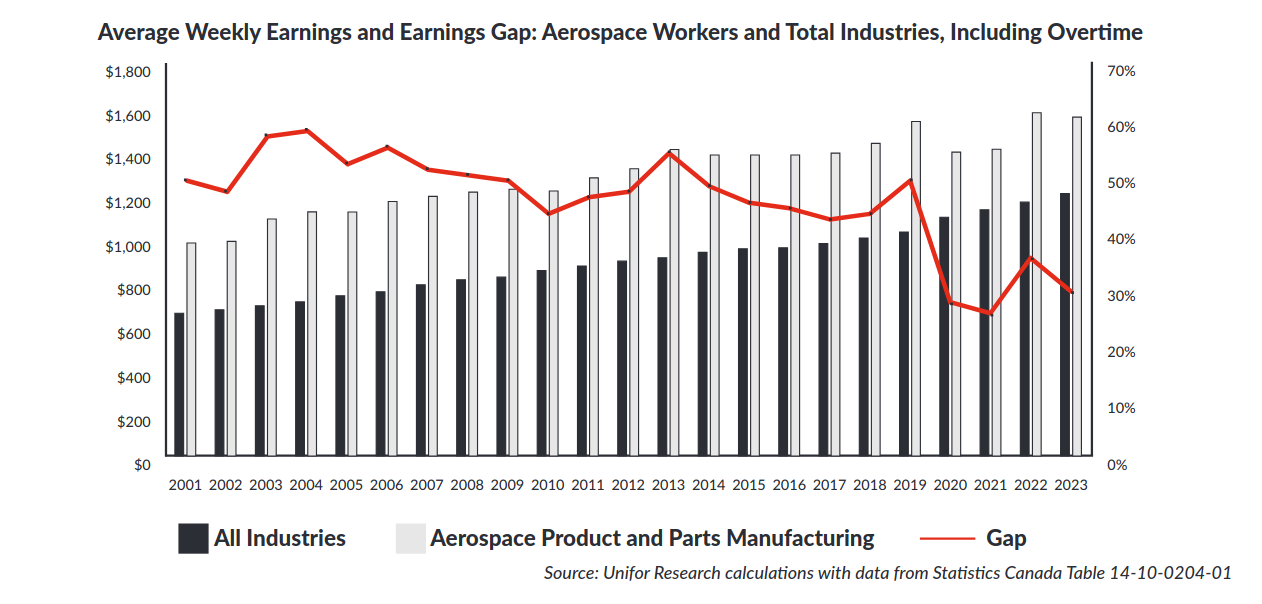

Finally, the erosion of wage advantages in the aerospace sector compared with Canadian workers overall—the average weekly pay premium has shrunk by 40% since 2019—is having a negative impact on attracting and recruiting the next generation of workers to sustain industry growth.

These stats distinctly inform the main concern of Unifor and the Unifor Aerospace Council that the lack of an industrial policy will cause Canada to let this incredible economic resource languish in uncertainty and go to waste. It is impossible to understate the important role governments must play in designing and implementing the policies and programs necessary to rejuvenate the industry for today’s workers and the next generation workforce.

Canada’s federal government currently takes a piecemeal approach to the aerospace industry. There is no doubt that important policies and funding envelopes exist including the Industrial Technical Benefits (ITB) program that ensures domestic aerospace suppliers are connected to large OEMs, and the Strategic Innovation Fund (SIF) that provides investment funding for a broad array of activities including R&D and increasing productive capacity.

These programs must be improved and expanded upon inside the new aerospace industrial strategy in order to ensure the country can fully capitalize on the achievements of the past and resources that exist right now to capture the growth of the future and build the good jobs and ingenuity Canada’s workforce is fully capable of.

Unifor’s vision for an industrial policy

Unifor’s vision for the aerospace sector includes several recommendations for government to help sustain good jobs through a resilient and forward-looking industry. It is comprised of four main pillars:

-

Pillar 1: Strategic Framework and Stakeholder Collaboration

-

Pillar 2: Workforce Attraction, Training and Adaptation

-

Pillar 3: Ecosystem supports and Made-in Canada Solutions

-

Pillar 4: Investments and Funding Programs

Pillar one makes it clear that Canada must create a strategic framework dedicated to the development of its aerospace industry and establish a multi-party aerospace development council that fosters collaboration among stakeholders.

Pillar two puts forward a plan to build a resilient workforce, ensure that new aerospace jobs are good, union jobs and that workers have access to the right training to maintain and expand the skills and technical expertise needed for the future.

Pillar three outlines the importance of supporting Canada’s aerospace industrial ecosystem and relying on made in Canada solutions to answer the country’s civil, search and rescue, forest fighting, defence aircraft and space technology needs.

Finally, pillar four describes the efforts Canada must take as an investment leader to conduct industry-leading R&D and secure new and existing industrial capacity that creates thousands of jobs for Canada’s current and future skilled workforce.

Ultimately, the creation and sustainment of good jobs in the sector is one of the most important economic benefits the industry delivers. The aerospace policy must work to maintain the premium on pay, employee benefits and high-quality training and development through policy tweaks and significant investment in training and getting out of the way of unionization.

For several decades, good unionized jobs in the aerospace and space industries have contributed to raising workplace standards in Canada’s manufacturing sector. Advances gained through collective bargaining have made it possible to attract and retain skilled labour who, to this day, constitute the foundational ingredient of our success.

Canada must not miss the opportunity to capitalize on past achievements and grow the aerospace legacy.

Pillar 1: Strategic framework and stakeholder collaboration

The Case for a National Aerospace Industrial Strategy

Considering its strategic importance, its close relationship with the research community, its security implications and an exceptional geographic reality, the evolution of the aerospace sector has always been characterized by sustained connections between the public and private spheres. This close relationship has enabled the Canadian industry to face global competition and overcome the challenges of rapid technological change, enabling it to remain at the forefront of developments in the sector, both in the air and in space.

Unprecedented Development of Industrial Capacity

Canada’s achievements in aerospace have been stunning, especially because they occurred despite significant shortcomings. Relatively speaking, the country is a middle-sized player in the industry on a global scale. The national market is small compared to those of the United States, China and Brazil, for example. It does not benefit from a developed military industry that acts as a subsidizing force in many other aerospace powerhouse countries. Furthermore, it does not have a major domestic commercial aircraft manufacturer. These are all advantages enjoyed by many of the dominant aerospace players elsewhere in the world.

Canada’s aerospace successes are based first and foremost on the talent, creativity and versatility of one of the most skilled workforces in the world. They are closely tied to government interventions made at key times. They are also the fruit of the favourable positioning and privileged relationships the country was able to maintain at the end of the Second World War that saw the aerospace industry benefit from a geopolitical and economic environment dominated by Canada’s main allies and partners. In a context marked by sustained demand, Canada repeatedly demonstrated its capacity to successfully build aircraft at scale and allow its workers to showcase their expertise.

At the same time, the industry could have soared even higher if a national strategy had existed as many competing countries had put in place. Since the last privatizations nearly 40 years ago, the Canadian government has sought to fashion a pragmatic, realistic approach to the industry adapted to global value chains, which has certainly produced results, but the ambition has not matched the industrial potential inherent in Canada’s current economic environment.

Several stakeholders are raising questions about Canada’s capacity to maintain its achievements and support the development of the industry under the status quo. The post-war world that saw Canada lay the foundations of its aerospace industry is a thing of the past. Today, strategic procurement, friend-shoring – the practice of shifting production and supply chains to countries that are political allies or have similar strategic interests – and building resilient supply chains are important government objectives that can be met with fulsome industrial strategies.

Strategic Awakening: The Struggle for Good Jobs

There have been profound upheavals in geopolitics, technology and, more recently, international trade. And the pace of these transformations is accelerating. New entrants are shaking up the traditional aerospace powerhouses, with the emergence of new alliances and boundaries.

Several states, including in Asia, the Middle East, Europe and Latin America, are cultivating new ambitions that translate into substantial investments in strategic industrial sectors. Their rapid economic growth provides them with new means they wish to leverage. In this regard, establishing or developing an aerospace sector is a highly desirable objective.

At the turn of the millennium, the Canadian government recognized the scope of the coming transformations and, in 2005, created a National Aerospace and Defence Strategic Framework that essentially developed a strategy for the sector. Its recommendations were never fully implemented. At the time, there was already a sense that Canada would be facing heightened competition in the coming years. Under its National Aerospace and Defence Strategic Framework, the government stated:

“…current success is no guarantee of future performance. The global aerospace and defence sector is shifting dramatically. To sustain Canada’s vision, industry and government must consider the new realities and must develop a renewed framework for collaboration—and a new national strategic framework for Canada’s aerospace and defence industries.”3

Seven years later, in 2012, the Aerospace Review made a similar observation, although with greater urgency:

“In an international economic environment where change has been breathtakingly rapid, the greatest risks are posed by complacency, and failure to adapt. Inertia would place in jeopardy one of the country’s most important industrial sectors and along with it, the critical economic, technological, and security benefits that flow from a healthy and competitive aerospace sector.”4

To its credit, the Federal government, under both the Liberals and the Conservatives, tried to address this new reality and worked to define strategic objectives with the goal of ensuring the sustainability of the Canadian aerospace industry.

The reports in 2005 and 2012 helped to identify the issues and possible solutions. This work bore fruit thanks to the support of inclusive consultations that brought together key sector stakeholders: government, industry, unions and academia.

The 2005 Strategic Framework articulated a 20-year vision and presented seven pillars focused on specific areas of intervention. It also led to the creation of the Canadian Aerospace Partnership, a multipartite organization responsible for identifying the industry’s strategic priorities as well as the public policies and initiatives to achieve them. The 2012 Review pursued these efforts by further developing several of these themes and emphasizing, in particular, operational dimensions and renewal of commercial approaches.

This work was a kind of golden age of strategic reflection for the Canadian aerospace industry. The recommendations that came out of it had substance and led to concrete improvements over the ensuing years.

Pressure Mounting to Preserve and Grow Canada’s Industrial Footprint

More than a decade has elapsed since the last federal strategic review. Canada has slipped from the fourth largest domestic aerospace industry in the world which it held at the turn of the last century, to sixth place.

While it would be unfair to claim that Canada’s aerospace industry is in crisis, the competitive environment in which it is developing is growing ever more complex and Canada is at risk of seeing its industry decline. The main trends identified more than 20 years ago are becoming entrenched. The resolute actions of Canada’s competitors are translating into considerable pressure.

Elsewhere in the world, emerging players who wish to carve out a place for themselves and well-established players who are seeking to rise in the ranks are taking deliberate and methodical steps, supported by the highest national political authorities to grow their own aerospace industries. While they have short-term targets, they are nevertheless following long-term development trajectories.

In addition to the country’s many existing initiatives, the United States just published its very first National Defense Industrial Strategy in November 2023.5 This reflects a significant change in how the country is addressing its industrial defence ecosystem, within which aerospace occupies a key role. The priority actions under this strategy include orientations focused on supply chains and workforce agility.

Meanwhile, France is pursuing its efforts under the Comité stratégique de la filière aéronautique (CSF), a tripartite governance structure that integrates various sectoral stakeholders, including unions. Its most recent Contrat de filière 2024-20276 sets out various development targets (decarbonization, strategic autonomy, job attractiveness, etc.), while CORAC, a government-industry consultative body dedicated to implementing a national research program for the industry, is coordinating a shared technological roadmap.

China has been making substantial investments to shore up its national aerospace industry and has been home to a national aerospace policy for many years. It recently announced the entry into service of the first C919 aircraft built by the state-owned aircraft manufacturer, COMAC and maintains strong long-term ambitions for the sector.

In 2018, the United Kingdom adopted an industrial strategy based on five pillars as part of its Aerospace Sector Deal.7 Sweden, with a population one quarter the size of Canada, continues to develop a remarkable integrated innovation system8 (Innovair) that places the strategic development of its industry at the heart of its actions and encourages the linking of civil and military initiatives. Even New Zealand adopted a strategy9 in 2023 focused on emerging aerospace segments within which the country feels it can hold its own.

Seeking a Strategic Vision

These development frameworks contrast with Canada’s approach. Canada’s goals for the sector lack definition and coherence. While many public measures exist, they are not aligned with a holistic and comprehensive vision for strategic development.

Private sector initiatives like the Aerospace Industry Association of Canada (AIAC) Gateway to Global Leadership10, Unifor’s regular advocacy for the sector and other unions and aerospace industry groups are attempting to fill the gap the government continues to leave, but it remains that there is no methodical public support infrastructure in Canada focused on the advancement of the national aerospace industrial ecosystem.

The Federal government had the opportunity to present its strategic aims and strengthen its support for the aerospace sector several times over the past few years but it has lacked ambition. The allocation of $1.75 billion over seven years in the 2021 Federal budget through the SIF was welcomed as was the Aerospace Regional Recovery Initiative (ARRI), a program implemented the same year to help SMEs in the aerospace sector recover from the COVID-19 pandemic. More recently, in June 2023, a $350 million investment was announced to support the Initiative for Sustainable Aviation Technology (INSAT), a program to accelerate the transition to more sustainable aviation through collaborative R&D projects in Canada.

Clearly, the Federal government cannot be accused of inaction, but it is problematic that programs and one-off investments are adding up without necessarily falling under clearly established guidelines. The SIF, which replaced the Strategic Aerospace and Defence Initiative (SADI) and the Technology Demonstration Program (TDP), two funding vehicles exclusively dedicated to aerospace, is a funding structure that is more general, and potentially less generous. Meanwhile, the ARRI, which came to an end in March 2024 after only three years of activity, does not represent a long-term development support measure.

Lack of Strategy Comes at a Cost

At present, most Canadian companies are not able to benefit from the structuring effects, economies of scale and predictability that an industrial strategy focused on greater stakeholder cooperation and integration could provide.

While linkages exist, opportunities for collaboration are underexploited. Relationships are frequently limited to fairly static supplier bubbles. R&D activities continue to be focused on a limited number of players with the result that there is insufficient knowledge dissemination across the industry more broadly including to SMEs.

This situation is partially exacerbated by the design of existing funding programs that are generic and transactional with rigid funding windows that simultaneously lead to redundancies and miss significant opportunities.

Moreover, while public defence procurement is bound by the ITB policy, the joint assessment of government needs and domestic industrial capabilities is not conducted at the front end of purchasing processes and the opportunity to co-develop products and solutions to government needs does not exist. Other countries provide that opportunity.

In short, the absence of national priorities and development targets leads to the piecemeal allocation of resources and decision-making that is too narrowly focused on local operational or commercial considerations. The consequence? Canada is not taking sufficient advantage of its industrial potential. As the global competitive environment intensifies, the opportunity cost Canada is paying by maintaining this posture is growing.

Despite the presence of more than 600 aerospace companies in Canada, the concentration of activities around a few major players means that the loss of one or two flagship production segments could have catastrophic consequences for the entire industry.

The devastating attrition of activities that recently occurred within the largest company in the sector in Canada should serve as a warning sign. The refocusing of Bombardier’s activities on business aviation triggered a major transition that ended with the sale of its three main airplane programs (C-Series, Q-Series, CRJ regional jets) to foreign entities (Airbus, Mitsubishi) and to one Canadian company (De Havilland). While there is no doubt that this offloading improved the company’s financial health, it came at a major cost in terms of job and industrial footprint.

Above all, Canada lost control over a clean-sheet design modern aircraft (C-Series) endowed with considerable development potential for the Canadian industry. For the time being, Airbus’s commitment to Canada is consistent with a long-term development vision. It nevertheless means that the fate of the C-Series, now known as the A220, will no longer be decided in Montreal, but rather somewhere between Toulouse and Hamburg where Airbus’s international and commercial headquarters are based.

What Is Canada Waiting For?

It is 2024 and Canada still does not have a dedicated industrial strategy for its aerospace sector. It cannot count on a stable, multipartite coordinating body that can reflect on and discuss sectoral issues, identify priorities and lead targeted actions. While Canada dithers, other countries are consolidating their positions and strategic infrastructure. Canada can no longer continue to operate with this vulnerability. It limits the demonstration of Canada’s capabilities and, ultimately, threatens the sustainability of the industry and leaves future growth and economic benefits on the table.

The Federal government needs to step up. It holds control over too many levers that fundamentally impact the industry, including jurisdiction over air transport and defence, oversight of fiscal policies, the ability to direct public funding for economic growth, foreign trade, and diplomacy to stand by the wayside. Canadian aerospace workers are now asking themselves: Is the Canadian government ready to adopt a strategic development plan for this key economic sector?

Recommendation 1: Create a National Aerospace Industrial Strategy

Canada must renew its vision and ambition for its aerospace and space industries. The federal government must develop a unified strategic development framework dedicated to promoting Canada’s industrial potential, consolidating its many existing sector projects and advancing new initiatives that attract jobs and investments.

This strategy must open the door to an exhaustive and ongoing assessment of the industry’s strengths, weaknesses and future opportunities. The development of clear priorities and the identification of the gaps that need to be filled will enable Canada to better channel its industrial development objectives in the short, medium and long term. This process must be informed by a cross-cutting approach that gives workers a voice.

The strategy must be based on a comprehensive approach to the industry that integrates civil aviation, search and rescue, defence and space. This would enable the Federal government to clarify its commitments to the industry and strengthen the coherence of its own policies as well as those of other levels of government, especially at the provincial level.

In particular, the strategy would make it possible to maximize the potential of the technological R&D ecosystem, find solutions to the many workforce challenges, heighten cooperation among key players in its cluster, facilitate strategic procurement, strengthen supply chains, improve SME resilience and growth and respond to the challenge of aviation decarbonization.

Recommendation 2: Create an Aerospace Industry Development Council

The federal government must put in place a permanent mechanism for multipartite dialogue, supported by the participation of the Canadian aerospace sector’s main stakeholders (governments, businesses, unions as well as research and training institutions) who will work together to create and implement the aerospace industrial strategy.

Adopting a strategy is one thing, implementing it is another. Any established vision or strategic approach needs to be assessed and adjusted on a continuous basis, and integrate a plurality of perspectives.

Like the Canadian Aerospace Partnership proposed in 2005 and the Aerospace Industry Advisory Council proposed in 2012, the creation of such a body is necessary and would provide the flexibility needed to address specific and emerging problems affecting the sector in a collaborative way.

Government must provide the infrastructure to develop, implement and operate the council. Stakeholders must commit to participating in the council in good faith with the core purpose being to grow and strengthen Canada’s industry to create good jobs and promote Canadian innovation.

This council will become a table where stakeholders can regularly discuss the strengths and challenges of the sector and plan coordinated activities to achieve continued success.

Pillar 2: Workforce attraction, training and adaptation

The success of the aerospace industry is highly dependent on a well trained, experienced and agile workforce. For many decades, that workforce existed in Canada, but over the last 10 years industry actors and governments alike took the existence of that workforce for granted and stopped investing in the next generation.

Between contracting out and offshoring, a reduction in on-the-job training, wage suppression strategies, the introduction of technology that eliminates career pathways and the slow erosion of funding for training in public institutions, the industry has become less attractive than ever to new workers.

Unifor locals in the industry consistently report an inability to attract and train a sufficient number of skilled workers as the main challenge to growing the industry in Canada. This challenge exists everywhere and is not for a lack of capable workers with the aptitude to meet the requirements of the industry. The challenge derives from the inability of the industry and educational institutions to meet workers’ needs including high quality training, secure employment, inclusive workplaces to name a few.

The loss of workers to different industries due to layoffs during the COVID-19 pandemic and the significant wave of retirements that is underway have led to a decline in the workforce. At the same time, technological change will challenge corporations to constantly train the existing workforce on new technologies they decide to implement.

In 2018, the Canadian Council for Aviation and Aerospace projected a need to hire 55,000 new workers by 2025 to keep pace with industry growth and to replace workers who are retiring or leaving the workforce for other reasons11. Much more work is needed to achieve this goal.

During the research phase of this policy project, local unions, industry representatives, innovation hubs and educational institutions all reported training-related challenges but they differed and sometimes conflicted from jurisdiction to jurisdiction. For example, some training institutions reported long wait lists and trouble finding skilled and experienced teachers for aerospace-related courses. Other training institutions reported empty seats in classrooms and an inability to fill the available spots. Innovation hubs and industry associations reported that funding timelines for developing new training solutions and programs are too short and often don’t cover necessary expenses such as administration and integrating lessons learned.

Workers said that employers were too focussed on finding people who were already trained instead of finding capable workers who could diligently go through a sophisticated training process and develop the needed skills. Workers also reported that current on-the-job training programs do not provide the right, in-depth training to get new workers ready for their career.

Together, two forces – a shrinking pool of workers and the need to upskill the existing workforce – pose an existential threat to the industry that continues to raise concern but has not been tackled on a large scale. One-time, bespoke solutions to workforce challenges are not the answer. Large-scale planning is needed to build a workforce that is trained and ready to design and build aircraft and space systems and an industry that creates jobs that meet workers needs and expectations.

Attracting and Retaining the Next Generation of Aerospace Workers

Attracting the next generation of workers to the industry to support current demand and future job growth will require a concerted effort to promote the high tech, exciting employment opportunities to the future workforce, protect the quality of those jobs through unionization, collective bargaining and workplace safety, and create a workplace that is free from harassment and welcomes underrepresented groups. To reach the heights everyone knows the industry is capable of reaching it must facilitate the arrival of a new, more diverse generation of aerospace workers.

Recommendation 3: Raise the profile of the sector for future workers

Industry, labour and governments must work together to develop a strategy to increase the profile of the industry among elementary and high school students and with teachers, guidance counsellors and parents. The strategy should include materials that introduce the exciting employment opportunities in the industry at an age when students are starting to make decisions about their future, highlighting potential career paths.

Efforts should be focused on schools in regions with an aerospace industry presence such as the Montreal-Quebec corridor, Toronto and southwestern Ontario, Winnipeg, Halifax and southwestern British Columbia.

Furthermore, access to the aerospace workforce should be enhanced through dedicated visibility initiatives similar to some recently seen in the health and social services sectors, as well as in construction. When combined with targeted scholarship programs, they can have a major impact on future students’ educational pathway decisions.

Recommendation 4: Foster inclusive workplaces

The industry must develop a strategy to create more inclusive workplaces to attract workers from underrepresented communities and facilitate workplace cultural change.

The workforce has and will continue to grow much more diverse. In order to continuously attract and retain the workers needed to drive the industry forward, Canada’s aerospace firms along with government, labour unions and educational institutions must develop a strategy that is focused on attracting and training the best and the brightest to the industry and then retaining these workers in a workplace that is not only harassment free but creates an environment where everyone is accepted and welcomed.

This strategy should include outreach that goes beyond the usual locations and a concerted effort to reach future workers who are women, people of colour, indigenous people, new Canadians and people with disabilities.

This strategy should include a plan for all participants – employers, training institutions and labour unions alike – to critically assess workplace cultures to ensure inclusive practices.It is often the case that institutions of all kinds are missing important opportunities to connect with new groups of people simply because they are using outdated outreach and retention strategies.

Recommendation 5: Protect and expand employment quality

The wage premium and employment quality are essential components of attracting workers to the industry and retaining those same workers once they are trained and experienced. Over the last decade, Unifor members have reported increased reliance on temporary staffing agencies inside their workplaces, contracting out of their work and offshoring of specific components of the work. The suppression of employment quality is one factor that leads to an inability to attract the talented workers the industry relies on.

Provincial and federal governments must introduce employment standards and labour laws that support the protection and expansion of employment quality and uphold decent work. Aerospace is a provincially regulated industry which means each province and territory will need to act to protect employment quality.

Every province and the federal government must make sure there are laws requiring equal pay for equal work so that paying temporary or part-time workers less than permanent or full-time workers is outlawed. This includes both hourly wages and additional benefits.

Governments must make it easier to join a union and develop the protections of a collective agreement through legislating card check certification and cracking down on anti-union behaviour.

Supporting World-Class Aerospace Education and Training Programs

Canada’s workers are among the most educated in the world. The aerospace workforce is no different. At the same time, diverse aerospace institutions from employers to trade unions to advocacy groups all report that the training ecosystem is in need of an upgrade. The funding squeeze placed on institutions by provincial governments, the reduction in spending on training by employers both on-the job and in training facilities and the difficulty attracting experienced instructors together act as a dead weight to the advancement of training in the ecosystem. Further to this, employers are often reluctant to place too much emphasis on training newly hired workers for fear of poaching by competitors. Finally, technological advancements require consistent training of the workforce in order to ensure they are capable of efficiently using the tools they are provided.

Recommendation 6: Build more dynamic and supportive training programs and partnerships

Government, educational institutions, industry associations and employers must facilitate the creation, customization and evolution of existing training programs.

Activities should include a review of current programs at schools, colleges and universities across the country to assess which are meeting the needs of students and if any need to be improved and industry led “micro” training opportunities or training tailored to specific workplaces that may have a new technology to integrate.

Employers need to reinvest in apprenticeship programs in the workplace and to provide on-the-job training in order to ensure workers are gaining the experience they need in a supervised environment.

Income supports and other wraparound programs are essential for workers who are required to attend upskilling programs off-site or off-the job.

The Aerospace HUBs in Montreal and Toronto are currently home to partnerships between industry and educational institutions that provide learning opportunities for students and industrial employers alike. These partnerships offer a combination of workforce development and research and product experimentation that is invaluable and must be fostered.

Recommendation 7: Address the shortage of teaching staff

Training centres are struggling to recruit and retain qualified teachers. The cyclical nature of the industry, which impacts registration levels, is making it difficult to maintain a stable team of trainers, with many being laid off during periods of marked decline. In this regard, the recent pandemic proved very challenging.

The disparity between the remuneration offered by public educational institutions, lower than that offered by companies in the aerospace sector, is another aggravating factor. Clearly, there is not much incentive for experienced employees active in the industry to join the ranks of a training centre.

But solutions exist.Introducing a program to alternate between teaching activities and work that would see industry lend resources to training centres over two, three or even five years, while maintaining the employment relationship and conditions (salary, pension, seniority, etc.) could, even on a very small scale, produce significant results.

Similarly, another option could be to maximize the potential offered by progressive retirement, enabling senior workers approaching retirement to split their time between the factory floor and the classroom. Facilitating this transfer of knowledge could prove highly fruitful for everyone involved while helping to reduce the staffing pressure on both schools and workplaces.

Implementing this kind of measure must be accompanied by a government wage subsidy to ensure industry workers who embrace such a teaching role, whether full or part time, are not penalized. It would also be crucial to make funding available to provide adequate support (educational specialist who provides guidance and expertise to improve teaching strategies and learning outcomes, support staff, etc.) to trainers coming from the industry so that they can adapt to a teaching environment, an important aspect in ensuring their retention.

Recommendation 8: Increase funding and flexibility of funding for training programs

Aerospace training is delivered in multiple locations including in vocational schools, colleges and universities but also through Aerospace hubs and other industry associations. Funding for training programs is provided by many different stakeholders including from federal,provincial and municipal governments or directly by industry. Often one program is funded by multiple groups.

While training and education related activities are of provincial jurisdiction, the federal government can play a more robust role in fostering a vibrant learning ecosystem by working with all stakeholders to increase funding and flexibility of that funding. The federal governement should send a strong signal to all of its partners by giving them access to sustained and predictable ressources, both financial and non-financial and not hesistate to leverage all of its capabilities to support aerospace training programs across the country.

Particular attention must also be given to the disparity in resources between large companies and SMEs within the framework of co-op work-study programs. Many smaller companies or those active in the MRO sector struggle to attract and accommodate these types of students due to challenges posed by the requirement for remuneration, limited hosting capacity, and lower visibility. More support is needed to ensure equitable access to hiring co-op students by supplementing resources for SMEs.

Recommendation 9: Develop and provide gap training

In 2023, Canada added Aerospace jobs to its list of in demand occupations opening up new pathways for internationally trained aerospace maintenance engineers to immigrate and contribute to Canada’s thriving aerospace sector. The program has largely been a success, however, there are sometimes gaps in training and experience that mean some internationally trained aerospace engineers who are new Canadians don’t have the full training needed to perform the work of AMEs in Canada – in other words their previous training meets some but not all of the requirements necessary to meet Canada’s qualification standard.

Stakeholders must work together to design training solutions for workers who have been internationally trained and have most of the skills to achieve a Transport Canada certificate but are missing some key qualifications. This training must safely and fully fill the training gaps to ensure these capable personnel get the training needed to meet the Canadian standard and take on jobs in the aerospace industry.

Ensuring Technological Changes and AI Integration Benefit Workers

Technological change has the potential to dramatically affect work in every industry in the country including aerospace. There is potential for technology to have both positive and negative effects on job quality. Technology has the capacity to disrupt career pathways, reduce or increase remuneration, introduce bias into processes, change health and safety performance, eliminate jobs, increase efficiency or increase workload and introduce opaque management techniques, among other effects.

Unifor’s risk-based framework for assessing the impacts of specific technological changes can guide local unions and groups of workers through a process of analyzing a new technology and developing strategies and programs that ensure their capabilities are augmented and their job quality not only does not erode but is potentially enhanced.

Recommendation 10: Require worker consultation in the design and implementation of new technology

Unifor experience has shown time and again that employers who consult with workers and implement their ideas during the design and implementation phase of technological change experience a more successful integration process. Workers are the experts at their jobs and should be providing input into how technology is developed and the most appropriate and efficient ways to be interacting with technology to improve outcomes. They deserve to be notified in advance and consulted on any technological change that will affect their work, the quality of their job or the management practices they are subject to.

Government, labour and industry must work together to develop a culture of consultation that respects the knowledge and expertise workers have developed regarding the job they perform and ensures they have an opportunity to understand how their work will be affected and mitigate negative outcomes on workers.

Recommendation 11: Design a robust program to support workers through transition

Workers need to be provided with opportunities to train and develop any new skills that are required to operate or interact with the new technology and need to see potential career pathways and opportunities for advancement.

A new aerospace development council must create recommendations for transition programs that provide training opportunities, on-the-job skills development, career enhancement and ensure gains from added productivity are shared between workers and shareholders. This must happen in a framework that puts worker stability at the core and promotes enhancements to job quality and technological change that augments workers’ capabilities without replacing them.

Pillar 3 : Ecosystem Supports and Made-in-Canada Solutions

Supporting and Expanding the Canadian Aerospace Industrial Ecosystem

From Newfoundland and Labrador to British Columbia, the aerospace industry reflects Canada’s diversity both in terms of capabilities and production. Unifor’s 11,000 active members in the industry proudly accomplish an extraordinary variety of tasks from machining parts for landing gear to producing satellites and maintaining aircraft. They have a unique perspective on the industry, its strengths and its weaknesses.

A broad range of targeted supports are required to help sustain Canada’s industrial aerospace ecosystem. Already underway, the work to implement a coherent set of key measures must be reinforced and would greatly benefit from the establishment of a national strategic framework. Increased efforts and resources must be devoted to strengthen innovation capabilities, develop new promising segments, notably in space, consolidate supply chains, enhance the growth and resilience of SMEs, support exports, help sustain Canada’s MRO sector as well as the civil aviation program of Transport Canada.

Recommendation 12: Strengthen Research and Development through collaboration and the implementation of appropriate support measures

The future of the Canadian aerospace industry largely depends on its capacity to innovate. Canada’s global positioning, the limited integration of its defence and aerospace sectors and the small size of its domestic market require the country to up its game. This requires a level of coordination within the industrial ecosystem that ensures collaboration between researchers and industry and between companies working on different component parts and final products.

The good news is that Canada has all the resources needed to succeed: university and college institutions with world-class researchers, teachers and students, government-supported R&D infrastructure, companies of all sizes working in a broad range of productive segments, experienced facilitator organizations and skilled workers.

We believe that the government has a key role to play in energizing the innovation ecosystem by reaffirming its industrial footing, identifying long-term development trajectories and giving it pan-Canadian scope. Unifor calls for an expansion of resources made available to Canada’s research and academic institutions, the National Research Council (NRCC) as well as cross-cutting groups like the Consortium de recherche et d’innovation en aérospatiale au Québec (CRIAQ) that foster collaboration amongst industry stakeholders.

Again, it is important to stress the extent to which the development of Canada’s innovation capabilities could benefit from a national industrial strategy. Adopting a framework that identifies clear priorities, sustainably funds initiatives that respond to predetermined objectives while promoting multisectoral collaboration and access to resources is key to boost successful made-in-Canada solutions and manufacturing.

Government intervention must set the tone and scope of this collaboration. To achieve this, various support mechanisms and programs can be implemented including research grants and government co-ownership of innovation projects that may help reverse the underinvestment in innovation.

Initiatives to support forward momentum in technological readiness levels (TRLs) can make the difference between ideas that never see the light of day and effective commercialization.

Better direct connections to Canada’s research infrastructure must become a differentiator for Canada’s corporate actors, particularly in the case of SMEs that have limited resources compared to large multinational groups. Government must also consider financing large-scale technological demonstrators to ensure they play a key role in ensuring Canadian subsidiaries can stand out and win important strategic projects.

Lastly, supporting the creation of innovation zones can contribute to strengthening the positioning of Canada’s aerospace hubs. The aerospace innovation zone that was recently launched in the Greater Montreal Area is an instructive example. This initiative brings together businesses, dynamic forces from the university research community, training centres and several other active players in Mirabel, Montreal and Longueuil with the goal of promoting collaboration in the industry.

Government must sponsor organizations that promote networking, consultation and cooperation among players in the aerospace cluster must serve as the basis of government-led actions.

Recommendation 13: Enhance Research and Development support measures for new aerospace technologies

Technological transformation is occurring in many segments of the industry. Artificial intelligence and robotization may make the news frequently but efforts to green the industry, develop drone remotely piloted aircraft systems and the rapidly expanding market for space technology are far more advanced and poised to expand in the near future.

For example, efforts are intensifying to decarbonize the aerospace sector. Several initiatives are already underway and are expected to multiply over the next few years as carbon-neutral goals become more specific: alternative fuels, alternative propulsion technologies, autonomous vehicles and automated radar technology, electric-powered vertical take-off and landing (eVTOL) aircraft, advanced materials and improved recycling and waste management techniques are some of the technological advancements currently underway. Responding to this imperative, Canada’s Initiative for Sustainable Aviation Technology (INSAT) created in 2023 to speed up the green transition in the aerospace sector is timely and must be resourced at a more robust level.

Remotely Piloted Aircraft Systems (RPAS) represent another sector poised for rapid growth and Canada is well positioned to benefit from this in both civilian and national security scenarios.

Finally, from the investments in NORAD and NATO to the LUNAR gateway project and exponential growth in low earth orbit monitoring and governance, the excitement surrounding the development and operation of new space technologies is not about to fade and will take on an increasingly important role within the Canadian aerospace industry in the coming years.

Recommendation 14: Support the resilience and growth of SMEs

The Canadian aerospace ecosystem includes just over 600 companies. More than 500 of them are SMEs. Their success depends on the existence of an inclusive industrial policy that is able to respond to their specific issues and challenges.

The role of SMEs in the aerospace cluster has greatly evolved over the past few years. Given the increased transfer of risk-sharing requirements across the supply chain, it has become more complex. OEMs have rising expectations. They want lasting, long-term supplier partners that are capable of developing complex components, taking on more sub-projects and intervening quickly when challenges emerge.

Meanwhile, government innovation and development support programs are often based on thresholds and selection criteria that are difficult for SMEs to meet. The application process is often long and costly and represents a challenge for SMEs with a limited number of specialized employees who can follow up on these types of tasks.

Moreover, the weight of government acquisition processes means that SMEs have difficulty piercing public markets, especially in the defence sector. Restrictions inherent to cash flow also hinder their capability and ambition, particularly for large-scale projects with long-term timelines.

There is a connection between this reality and the difficulties SMEs have in increasing their size, their market presence, their organizational resilience and, ultimately, the working conditions of Unifor members. The COVID-19 pandemic highlighted the vulnerability of smaller businesses and Canada needs to focus on growing their importance.

Considering the key place SMEs occupy in the Canadian aerospace industrial structure, a flexible and diversified approach is needed to promote their development. Access to financial resources is a central issue and SMEs need to be able to benefit from permanent funding and assistance that, while integrated into an overall support infrastructure, will be able to respond exclusively to their needs.

To integrate a broad cross-section of their needs at the front end of policy development, government must create a dedicated body within the previously mentioned Aerospace Industry Development Council and similar to the Comité aéro PME12 within the CSF in France.

Greater SME resilience requires greater promotion of R&D, a development vector that directly influences their agility and can have a decisive impact on their future in a context of increased integration and complementarity with the big industry players. That is why it is important to strengthen SME access to the services and equipment of public research centres, in particular for applied research, testing, experimentation and demonstration projects, and to facilitate their integration into international innovation networks.

Lastly, SMEs must be able to bid on public procurement tenders, in particular as part of demand-oriented strategic procurement, and be supported in the process to comply with more exacting and onerous security and defence standards.

Recommendation 15: Strengthen supply chains

The reliability and transparency of supply chains that feed production in Canada need to be improved. The challenges of supply chain disruptions were brought up repeatedly during the work and discussion workshops with members of Unifor’s Aerospace Industry Council. The difficulty in obtaining various parts and components needed for the manufacturing process was a significant problem with several negative impacts.

Members reported they lost significant working time when final orders fell below anticipated levels and employers lost revenue. In some cases, temporary layoffs were imposed. Production rates were also undermined, while operations that were paralyzed as a result of missing parts had to be resumed at an accelerated pace. This upheaval had repercussions for the quality of workplace support and training for new employees.

In addition, intensified merger and acquisition activity in the supplier base has reduced the supplier options available to OEMs and further eroded the industry’s resilience.

Governments must adopt a whole-of-supply-chain approach to attracting investment in the sector that keeps re-shoring the manufacture of component parts at its core. Government must identify the pathways through which component manufacturers can bring work back to Canada or build greenfield projects in order to build a resilient supply chain that is not subject to the volatility in the shipping industry or decisions of other countries’ governments.

Recommendation 16: Support exports and champion Canadian products internationally

The vitality of the Canadian aerospace industry depends in large part on its capacity to sell its products outside the country. Close to 80% of Canadian aerospace production is exported, for a total value of $19 billion in 2022. The aerospace sector alone represented 13.5% of the total value of Quebec exports in 2023.13 The future of Canadian aerospace workers is intimately tied to maintaining these important connections with foreign markets.

The Canadian government must remain abreast of the evolving commercial environment and current competitive dynamics as they evolve. Whether it is sector understandings on export credits or other types of arrangements, Canada would benefit from supporting the creation of a level playing field with other jurisdictions so that Canadian corporations can take advantage of international growth opportunities.

At the same time, Canada must make sure to offer all possible latitude to its export assistance agencies in order to support Canadian-based businesses, in particular with respect to sales financing, while ensuring the development of a more coordinated export support system that is focused on stakeholder collaboration including between government departments, support organizations and businesses. This approach would mirror efforts undertaken in other parts of the world, namely, in France, Sweden and the United Kingdom.

Lastly, it is important to focus on strategic economic diplomacy that places the emphasis on Canada’s distinctive strengths. The proximity that exists between the political spheres and aerospace industry development strategies requires us to put high-level political support provisions in place to promote the competitiveness of Canadian businesses on international markets. In support of these efforts, stimulating the development of solutions through its national industry and acting as the anchor buyer is the strongest message a government can send to its trade partners.

Recommendation 17: Develop a “Service-in-Canada” policy to grow maintenance, repair and overhaul activity

The value of maintenance, repair and overhaul contracts over the life of an aerospace program can often exceed the total cost of an acquisition. Aerospace maintenance, repair and overhaul activity created $4.2 billion in GDP in 2023, comprising 30% of the industry’s direct economic activity. MRO activities are carried out on government owned and military aircraft as well as civil aircraft operated by commercial airlines across the country.

Canada must implement a “Service in Canada” policy that ensures domestic firms perform overhaul and maintenance and inservice work on aerospace equipment owned and operated by federal, provincial and municipal governments. These aircraft are in-use to support broader public goals such as defence, firefighting and coast guard related tasks and can also be put to use supporting robust safety standards and high quality jobs for workers.

Recommendation 18: Reinvest in Transport Canada’s Civil Aviation program capabilities

Transport Canada’s Civil Aviation program capabilities constitute a major strength for the industry. This program represents a strategic asset crucial to maintaining the country’s enviable reputation in aerospace and air transport reliability and security.

Through its leadership, the organization opens up opportunities for the industry in international markets where most of its production is sold. Canada’s renown in the area of security is, in itself, a selling point and facilitates acceptance and recognition by international regulatory agencies of solutions designed and manufactured here.

These strengths enable Canada to set itself apart from other countries. The country’s capacity to domestically design, develop and certify aerospace products according to international standards, accelerate the marketing of innovative ideas and contribute to developing new standards in collaboration with counterparts from other countries to be vigorously protected. Moreover, Transport Canada’s ongoing involvement in international regulatory agencies is crucial for maintaining Canada’s credibility and should be encouraged.

Enhancing Transport Canada’s role requires investments to preserve these strengths and increase the agility and speed of the organization’s operations. Transport Canada needs to be able to collaborate strategically with the aerospace industry in all regions of the country. Beyond modernizing its technological infrastructure, these investments should make it possible to hire more staff, train them and retain these highly skilled workers through good salaries and social benefits.

Recommendation 19: Support the Canadian space sector

Space technology is a critical component of government infrastructure and source of Canada’s ability to maintain its sovereignty. It is also a new frontier in R&D for all kinds of products that could one day benefit humanity. Communications satellites monitor climate change and can assist in delivering remote health care. Space robotics will assist astronauts to explore the moon and to transfer to and from the International Space Station. Federal and provincial governments must ensure that space technology is given equitable attention and support to the rest of the aerospace sector, including through funding and procurement initiatives and as a part of the strategy and development council.

Canada has been a leading actor in space technology for decades. The space subsector has moved from a niche market to mainstream. From communications and reconnaissance satellites to space robotics and the governance capabilities to manage new frontiers, Canada is positioned to lead the world..

The Canada Space Agency and Canada Space Strategy promise to play a vital role in growing the space sector. Both must become a sub-component of the Aerospace Strategy as well.

Using Public Procurement to Strengthen the Aerospace Industry

Government must focus their attention on growing made-in-Canada solutions in aerospace. The first step is to recognize and acknowledge the capabilities that exist in the sector. The second step is to mobilize the resources in multiple ministries and programs necessary to ensure made-in-Canada solutions are properly funded and promoted to both domestic and international customers.

Project trajectories in aerospace, space and defence sectors should be reviewed with an eye towards maximizing economic benefits to Canada and building Canada’s industrial capacity. The procurement dimension, particularly when these products respond to proven and recurring needs of Canadian citizens and public institutions, is underutilized and underdeveloped in Canada. Unifor sees this as a massive and glaring weakness that must be addressed.

Strategic utilization of public procurement could be a strong catalyst of the aerospace industry. The Canadian government is poised to spend no less than $75 billion on defence and space exploration projects in the next decade alone. From NATO and NORAD upgrades to satellites that study climate change from low-earth orbit, there are a number of projects that could be successfully fulfilled by Canadian companies if adequate measures are put in place to ensure collaboration on product development.

Defence and security-related contracts provide undeniable advantages to the industrial ecosystem. This is made clear in the United States, in Europe where favourable conditions ensure domestic companies are able to fulfill government procurement contracts. In Canada, these procurements will include a wide range of purposes that should be leveraged to maximise benefit to Canada whenever possible.

Such projects are typically exempt from trade agreement restrictions that prohibit government’s from imposing domestic or local content requirements in major purchases of goods and services. They also offer stable, usually long-term, revenue flows that are particularly useful for offsetting the cyclical fluctuations of the civil aviation market and open the door to many opportunities for technology transfer.

For example, the fly-by-wire control systems developed by Embraer for its KC-390 military transport aircraft benefitted its E2 single aisle aircraft program, while Airbus’s advances in composite materials for the A400M were used on the larger version of the A350 long-haul aircraft. In both cases, early investments in innovative technology through domestic R&D led to larger advancements in commercialized projects. Canada should be creating this dynamic in its domestic industry as well.

A Beneficial Strategic Relationship

The latest version of the Quebec Aerospace Strategy unveiled in 2022 acknowledged the industry’s low exposure to the public sector procurement market and made it a development priority. The diversification of activities in defence and security was identified as a source of resilience for the industry. The document, produced when the effects of the health crisis were waning, also noted that the businesses that fared best during the COVID-19 pandemic were those that had a diversified customer portfolio.14

Canada’s inability to fully leverage this key sector is not a new phenomenon. The deficiencies in the Federal government’s procurement activities have been known for a long time. In 2012, the report by the Working Group on Aerospace Related Public Procurement noted no less critically that “Of all the countries examined during the analysis of global practices, Canada seems less inclined to take concerted actions to support its own indigenous defence industry.”15

Clearly, there is a limit to what the Canadian industry can accomplish to respond to the needs of the Royal Canadian Air Force (RCAF) given that it does not have, for example, a fighter jet or a heavy transport plane program. Moreover, the privileged relationship between Canada and the United States that opens considerable doors to the U.S. market for Canadian companies also requires the country to strike a balance in how it promotes its own industrial base in terms of procurement.

There was once a much closer relationship between the State and the aerospace industry, reaching its zenith during the Second World War, when the Canadian government nationalized De Havilland in 1942, created Canadair as a Crown corporation in 1944, and provided massive support to Avro Canada’s operations. Various development programs emerged in the ensuing years, including for Avro’s CF-100 Canuck and CF-105 Arrow, and Canadair’s licenced production of the F-86 Sabre and CL-89 surveillance drone.

This symbiotic relationship greatly contributed to structuring the country’s aerospace industry and paved the way for its development in the following decades. The privatization of De Havilland Canada and Canadair in 1986 marked the end of this type of public involvement and the beginning of a more distant and transactional relationship between the Canadian government and these companies.

Benefits Policies

Coincidentally, the year 1986 also marked the creation of the first Canadian Industrial and Regional Benefits (IRB) Policy to ensure that major government contracts, in particular in the defence sector, contributed to Canada’s economic development. The policy also sought to better distribute industrial development across the country’s various regions, to strengthen technological capability and to create jobs.

The policy reflected a strategic shift by the Canadian government, which realized that the industry’s future lay in its integration into global value chains, which were dominated by multinationals, most of them international.

In many respects, this pragmatic and prudent approach served Canada well. The policy strongly influenced Boeing’s operations in Manitoba, leading to substantial investments in local manufacturing capabilities and workforce development. It promoted greater presence of internationally owned companies in Canada like Pratt & Whitney Canada, Lockheed Martin and General Dynamics Mission Systems–Canada. It also sent a clear message to Canadian companies in an environment marked by the growing offshoring of production activities.

In 2014, the IRB Policy underwent major review and was renamed the Industrial and Technological Benefit (ITB) Policy. This strategic reprogramming was motivated by a desire to strengthen the quantity, quality and impact of the benefits.

The introduction of a value proposition, within the ITB Policy, required bidders to detail the economic benefits their projects would deliver to Canada. The Canadian government also sought to provide greater direction to the scope, duration and nature of the Policy’s benefits by emphasizing innovation, increased SME participation, alignment with Canada’s industrial priorities and strategic objectives, prioritization of key industrial capabilities (KICs) and, ultimately, a better assessment of its performance through stronger accountability.

According to Innovation, Science and Economic Development Canada (ISED), on average during the 2017–2021 period, the ITB Policy contributed close to $5 billion to GDP and supported more than 44,700 direct and indirect jobs per year in Canada. The most recent statistics show that of the 715 participating organizations, 63% are SMEs. In 2023, the aerospace industry captured half the transaction value (49%), a reflection of the importance of this policy for the sector. Since its implementation, the value of economic activities generated, in progress and to come, is $48.1 billion.16 While these aggregate statistics—the only ones publicly available—are impressive, a more detailed analysis reveals a less flattering portrait.

Limitations of the Model

In 2022, an analysis conducted by the Office of the Parliamentary Budget Officer (OPBO) based on disaggregated data, revealed gaps inherent in the transactions under the ITB Policy between 2015 and 2019.

Despite the Policy’s claim of prioritization based on capabilities and key areas (for example, SMEs), the analysis revealed that credit multipliers that were supposed to accentuate them only represented 0.8% of total transactions. The proportion of indirect benefits regarding work not linked to procurement represented close to half (47.1%) of the total transaction value in dollars.

While the number of recipient SMEs identified by ISED seemed high, they ultimately received only a fraction (12%) of the transaction value, with a higher proportion (60%) than the overall average being indirect. Lastly, the work of the OPBO showed that the enterprises belonging to Canadian interests represented only 30.8% of the total transaction value in dollars with major business partners.17

This data contrasts with the more promotional tone of the ITB Policy’s annual report issued by ISED. It highlights the need to strengthen existing accountability mechanisms that do not make it possible to properly assess the concrete application of value propositions. The two current tools at our disposal (Annual Report, Report on Contractor Progress) are insufficient. A more granular perspective is required to better identify best practices, compare the benefits value and develop opportunities for improvement.

The OPBO evaluation of the broader impact of the industrial and technological benefits program highlights the following point: however elaborate these measures may be, they cannot become a substitute for an actual industrial policy.

Vigilance and exploration of complementary approaches are still in order. In short, the issue of Canadian government strategic support for its aerospace industry through defence procurement should not be restricted to these benefits programs.

An excerpt of the report by the 2012 Working Group on Aerospace Related Public Procurement provides a good summary of the challenges of the implementation of a benefits policy and the limitations of a transactional approach in the absence of an overall industrial strategy:

“The concept of having an IRB policy is potentially a powerful tool to achieve national objectives which need to be enshrined in an aerospace and defence industrial strategy/policy. Unfortunately, in the absence of these policy objectives, the IRB policy has been expected to achieve impossible goals. Indeed, it can be argued that the very existence of the IRB policy may have lulled the government into a false sense of achievement. In fact, it seems to have exacerbated a difficult situation by leaving ministers and government officials with the impression that they need not put effort into developing focused strategies to generate Canadian industrial strength and economic well-being because the IRB program would achieve these objectives. The reality is that the procurement strategy identified at the front end of a program has far more impact on economic outcomes and jobs than an IRB program, applied on the back end, in the absence of an accompanying industrial strategy.”18

Canadian Multi-Mission Aircraft

Recently, the conclusion of the acquisition process for the Canadian Multi-Mission Aircraft (CMMA) project highlighted the growing malaise around how governments view the Canadian aerospace industry’s contribution to the needs of the Royal Canadian Air Force (RCAF). The CMMA project offered a unique opportunity for Canada to develop a sovereign platform in one of the few niches of military aerospace (ISR/ASW)19 for which it had all the required capabilities. By acting as the anchor buyer, the federal government could have contributed to the emergence of a promising new program and opened export opportunities.

Through lack of vision and planning, a ready-to-use U.S. designed aircraft was chosen instead of an over-the-counter contract worth over $6 billion. The potential contribution of Canadian companies was not even analyzed until after the procurement was complete. This solution will respond to the needs expressed by the RCAF. It will generate benefits, the $240 million in investments announced20 by the company that won the contract in the Montreal area testify to this. However, it is clear that had this been addressed differently—based on a front end strategic and collaborative approach— this project could have created even more work for Canadian suppliers and had a fortifying effect on the industry. This type of missed opportunity seriously hampers the development of Canada’s aerospace industry.

Demand Oriented Policy

With respect to the gaps identified in the ITB Policy and the deficiencies that have been noted in how the government supervises and manages military aerospace equipment purchasing processes through Public Services and Procurement Canada (PSPC), the Department of National Defence (DND) and ISED, it seems clear that improvements can be made to the framework that is currently in place. After decades of liberalization and the massive withdrawal of government involvement, the current policies may be too focused on supply. As a result, they neglect the importance of the potential benefits of a strategic procurement approach identified at the front end and inspired by demand-oriented policies.